Mixed-Income Public Development Model

The affordability achieved under the Mixed-Income Public Development Model is enabled by three key elements:

- A revolving loan fund to provide a portion of construction financing;

- Low-cost permanent financing enabled by existing HUD and Treasury programs; and

- Mission-aligned mezzanine financing to bridge gaps between construction and

permanent financing.

Additional considerations beyond the financing sources themselves include:

- Governance in a majority public ownership structure; and

- Asset management responsibilities for the public sector.

In this section, we describe each of these elements in detail and show how they fit together to deliver publicly owned, mixed-income housing.

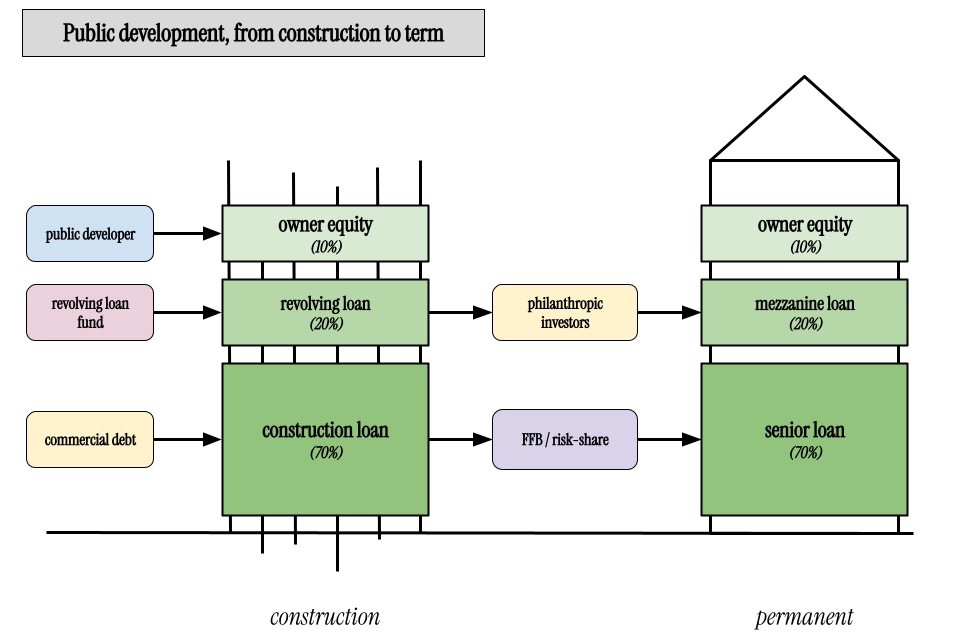

A Revolving Loan for Construction Financing

Financing multifamily housing development typically occurs in two phases. The first, construction financing, involves equity and debt developers assembling to complete pre-development and construction activities. In a market-rate transaction, most costs are paid for by a short-term (12- to 18- month) construction loan from a bank covering the majority of pre-development and construction costs. The remaining costs would be covered by either the owner’s equity or a private equity investment. Second, once projects are built and leased, projects convert to permanent financing, paying off and replacing construction loans with longer-term notes. Because there is less risk involved with a completed, occupied building, permanent financing carries lower interest and is typically paid for out of the net operating income of the building (i.e., rental income less expenses).

In the current high-interest-rate environment, construction loan sizes are decreasing. In lowerinterest- rate environments, construction mortgages might cover two-thirds of a project’s cost. In today’s conditions, that loan-to-value ratio can be much lower, closer to just 50 percent, requiring developers to rely on private equity investments to cover gaps, which often come with expectations of double-digit returns, driving up overall construction costs.

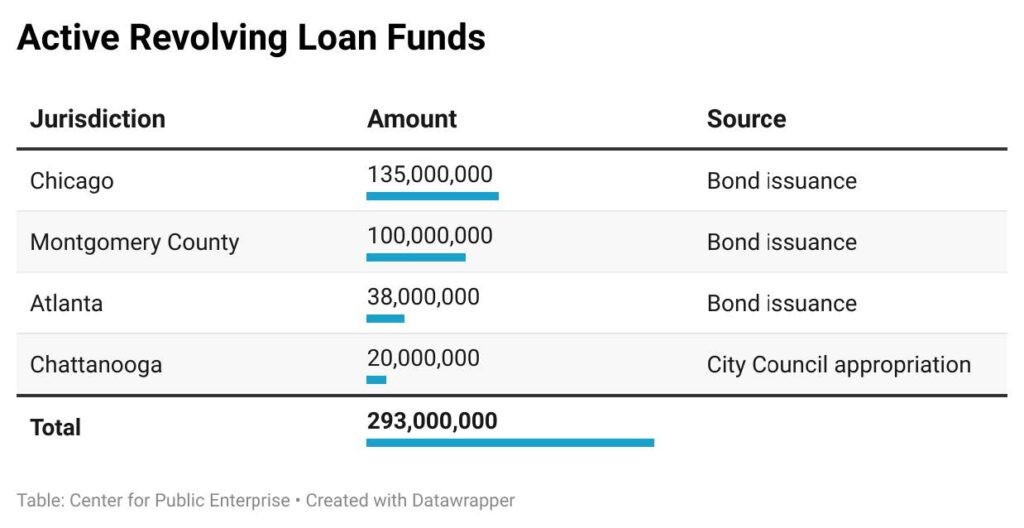

The public mixed-income development model overcomes this hurdle by replacing private equity investment with funds from publicly funded revolving loan funds. Revolving loan funds provide roughly 20 percent of the construction costs and then are replaced when the project converts to permanent financing, allowing the fund to make further investments.

Low-Cost Permanent Financing

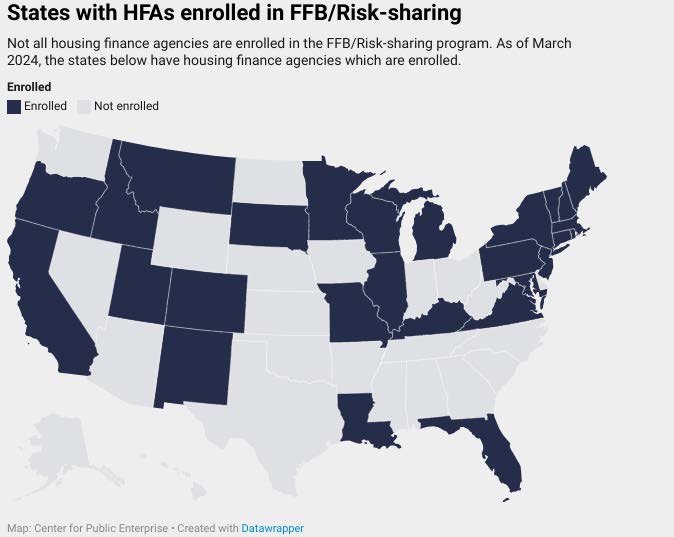

At stabilization (after the construction and lease-up of a property), senior debt is converted to a permanent mortgage. Here projects can leverage low-cost public financing through programs such as Section 542(c) Risk Share Program. Risk Share is a federal program allowing the Federal Housing Administration (FHA) to partner with qualified state Housing Finance Agencies (HFAs) to share the risk on mortgages issued by the HFA. The Risk Share program provides credit enhancement to HFA bond and debt issuances through FHA mortgage insurance, resulting in lower borrowing costs. HFAs are then able to pass on these savings to multifamily borrowers, resulting in lower financing costs that promote the development of affordable housing. Loans made under the program can finance up to 80 percent of the project’s total cost with competitive interest rates due to reduced risk.

There is an add-on to the Section 542(c) Risk Share Program wherein Treasury’s Federal Financing Bank (FFB) purchases Risk Share loans. This provides a major advantage to participating agencies; instead of having to source capital for loans from the market or their existing balance sheet, they can have those loans funded directly by FFB. The key advantage of Risk Share paired with FFB financing regards enabling sources of permanent financing that do not rely on tax-exempt bonds, which may be scarce depending on the state. Projects using FFB/Risk Share for permanent financing do not trigger prevailing wage requirements because the federal government is not assisting with the construction phase, but all Risk Share projects are required to provide either 20 percent of units at 50 percent AMI or 40 percent of units at 60 percent AMI and adhere to federal environmental requirements. Generally, the interest rate on FFB/Risk Share loans equals the 10-year Treasury rate plus 100 basis points. Over the last eight years, interest rates on FFB loans made for new construction and substantial rehabilitation have ranged from 1.89 percent to 6.32 percent.

Although the Risk Share program is described as a program for housing finance agencies, regulation defines a housing finance agency as any public body empowered to finance housing activities. This leaves open the possibility that other state-chartered entities, such as public housing authorities, could access Risk Share and FFB directly. The Center for Public Enterprise is currently working with several jurisdictions to explore different methods of accessing the program.

Recent changes to the Risk Share program have made it even more useful for new development. The Treasury recently announced it is instituting an interest rate “collar,” to the program to mitigate the risk posed by interest rate variation between the construction and permanent financing periods. Between the start of construction and the acquisition of a permanent mortgage, interest rates can fluctuate — sometimes significantly. If a developer builds a project when rates are 5 percent, but completes it when rates are 8 percent, they might find themselves in a bind. With the new change, when a project is approved for FFB/Risk Share, it will lock in a so-called rate collar, providing certainty that the eventual rate on the permanent mortgage will be within a specified range, or collar.

While Risk Share and FFB bring significant benefits, it is possible to execute the mixed-income public development model with other permanent financing sources. For example, if a state has excess bond volume cap, permanent financing could be arranged via a tax-exempt bond issuance. Financing can also be provided through conventional private bank products, if the administrative and compliance requirements of using FHA Risk Share do not outweigh the value of lower interest expenses, particularly if the business cycle is in a stage in which interest costs are less of a cost driver.

There is a long history of using public financing for mixed-income projects. HFAs have successfully financed 80/20 deals (80% market and 20% affordable) as far back as the 1970s using tax-exempt bond financing. The challenge has always been that these projects pull from a finite source of tax-exempt bond volume, and states often, and rightly, prioritize 100 percent affordable deals with LIHTC over mixed-income projects. Using FFB/Risk Share allows projects to proceed even when tax-exempt bonds are oversubscribed.

Tax-exempt bond issuances can also be considered as a source of lower-cost permanent financing with fewer programmatic limitations. However, municipal bonds can come with challenges such as limited non-issuer ownership, and variability in costs due to the effects of the financial capacity and rating of the issuing municipality. Using tax-exempt bonds would also use bond volume cap, which may be better allocated to other financing activities such as single-family first-time buyer programs and various other multifamily projects.

Mission-Aligned Mezzanine Financing

At the conversion to permanent financing, projects are typically able to secure senior loans with more favorable loan-to-value ratios than the loan-to-cost they received on construction financing. In some cases, this allows permanent loans to pay off the revolving loans.

In projects where permanent loans are not large enough to completely pay off construction loans, the model typically relies on a source of mission-aligned capital — most often from community development financial institutions (CDFIs) or philanthropy—to pay down construction loans. The Montgomery County Housing Opportunities Commission typically underwrites its projects conservatively under a worst-case scenario in which projects receive a roughly 10-year mezzanine loan at 10 percent interest. In practice, when HOC goes to market for financing, it can typically secure lower interest rates because it has an attractive product to offer: moderate returns on investment backed by real estate with paying tenants in high-opportunity areas. HOC has historically been able to secure terms below their “worst-case” benchmarks.

Communities seeking to replicate this model could turn to local philanthropy as a potential lender for the mezzanine debt at conversion to permanent financing. There is natural alignment between public mixed-income housing projects and philanthropy seeking sensible investments that have immediate impact on their local communities. More broadly, a national source of consistent mezzanine financing to replace a revolving loan fund investment could help this model expand into areas that would otherwise struggle to attract such capital. If replacement mezzanine financing for stabilized assets is not available at a reasonable cost, jurisdictions could leave the low-cost construction loan in place for a longer period or replace it with another source of local financing. This would reduce the leverage on the production fund by slowing its revolution but would still generate valuable new affordable housing outside of what federal subsidy can support.

Certain entities have the capability to combine these financing mechanisms with property tax relief, further contributing to affordability and allowing the development costs to “pencil”. The National Housing Crisis Task Force has published an additional tool on this subject, Right-Sizing Property Tax Incentives to Increase Housing Affordability.

Governance Structure: Public Ownership

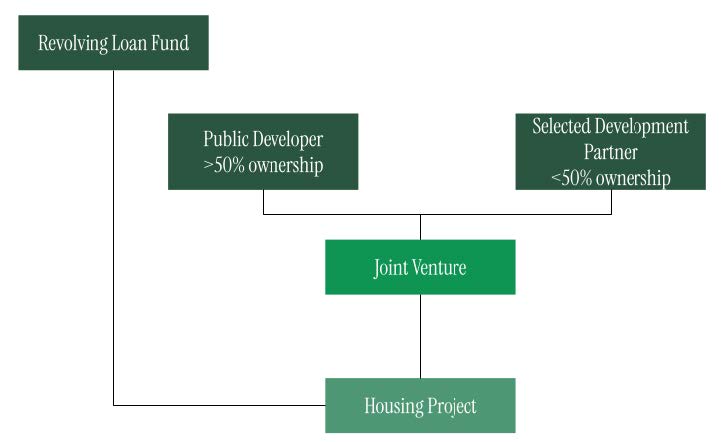

Majority public ownership, in contrast to other public-private arrangements, leaves control of the affordability of housing units in the public sector’s hands and ensures that the public sector sets the policy regarding how units are developed and managed. It also allows public retention of value coming from these projects as they appreciate over time and reinvesting that value in additional affordable housing developments throughout the community.

In Montgomery County’s case, the public ownership entity is HOC, which serves as both a PHA and local housing finance agency (HFA). HOC seeks to maximize affordability on all its projects. All market-rate units are voluntarily rent stabilized (rent increases are based on rental Consumer Price Index), and income-restricted units in the property are maximized against cash flow requirements. In structuring projects, HOC will add affordable units, or deepen their affordability, to the greatest extent possible while still maintaining a financially self-sufficient building.

Perhaps more importantly, the county can add additional affordable units at no cost in the future. When mixed-income properties are refinanced, for example, in 10 years, any reduction in annual debt service costs can pay for the addition of more income-restricted affordable units in properties. Without majority public ownership, this is significantly more difficult especially when it reduces the profitability of properties — a challenge for a private, for-profit entities with fiduciary responsibilities to maximize profit.

Under the mixed-income public development model, the public entities bring tremendous value to projects — and retain that value. In HOC’s case, the county often brings low- or no-cost land, significantly reduced cost capital, and reduced or eliminated property taxes to projects. In exchange, HOC takes majority interest in the properties. And, despite early concerns that developers would balk at the proposition of not owning their properties outright, HOC has so far been inundated with requests from developers to partner on projects.

To initiate projects, public entities enter into joint venture agreements with private development partners, with the public entities taking majority stakes. Each property is set up as its own individual Limited Liability Company (LLC). This insulates the parent company or sponsor from lawsuits or liabilities stemming from individual projects. Housing authorities or public entities would negotiate development agreements covering items including, but not limited to: ownership structure, land and site control, development responsibilities and fees, asset mana gement and resident service agreements, cash flow distribution splits, and decision-making processes.

Public authorities and private developers would also negotiate options for the private partners’ exit from the deal. This could take various forms, including developers being bought out after a specific amount of time or having an option to convert their upfront equity to debt.

Asset Management

Once a property is built and stabilized, agencies have the flexibility, as they do now, to provide their own property management or contract with an outside entity for property management services.

Moving toward this type of model could represent a change in the business operations for some PHAs, which for a long period of time were permitted to centralize accounting and property management, as opposed to adhering to project-based methods more common in the private sector.

It will also require stewardship of these assets as true mixed-income communities. While appearing simple on the surface, getting the asset and property management right for these projects requires thoughtful and attentive implementation that goes beyond simply the financial performance of buildings.